One of the more unique provisions in the One Big Beautiful Bill is the introduction of a new Federal Baby Savings Account designed to encourage families to save for their children’s future expenses, including education and healthcare.

The initial $1,000 deposit is funded by the government and future contributions can be made by parents, relatives, and parental employers, allowing for collective support in building savings.

Funds in the account can grow tax-free, providing a significant advantage for long-term savings growth.

How the Program Works

Eligibility

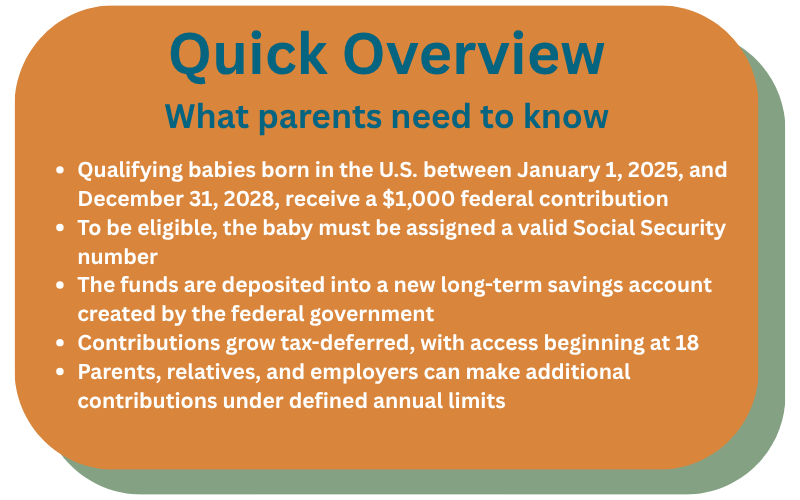

To be eligible, the child must be born in the United States between January 1, 2025, and December 31, 2028. Extension of this window is subject to future legislation. Eligibility is automatically triggered when a tax return has been filed listing the child as a dependent. At least one parent or guardian must have a valid, work-eligible SSN.

- Children born before 1/1/25 are not eligible.

The Account

Accounts can be set up by the parent or guardian at a qualifying institution or the Treasury Department may create the account on behalf of the family. In both cases, a one-time deposit of $1,000 will be made by the federal government, investing the funds into a low-cost U.S. stock index fund. The account remains custodial until the child turns 18.

Contributions & Withdrawals

- Parents and family members can contribute up to $5,000 annually, per child. This limit will increase to account for inflation. Contributions are not tax-deductible, but investment growth is tax-deferred.

- Employers may contribute up to $2,500 per year per child. This income is generally tax-free for the employee but does count toward the $5,000 contribution limit.

- No withdrawals before age 18.

- At 18, the account transitions to an IRA-style account with similar rules and exceptions.

- Qualified uses may include:

- Higher education

- First-time home purchase

- Job training

- Small business startup

- Adoption or childbirth expenses

- Unqualified early withdrawals may be possible but will be subject to taxes and penalties.

What’s still unclear?

While the general framework has been established, several important implementation details remain pending:

- IRS Guidance: Specifics on how the accounts will be managed, opened, and reported are not yet finalized.

- Financial Institutions: A list of approved institutions that will administer the accounts has not been published.

- Fund Options: Exact index funds eligible for investment have not been named.

- Conversion Mechanics: Details on how the account converts at age 18 (and how distributions are tracked) are still forthcoming.

- Outreach and Enrollment: It’s not yet clear how automatic enrollment will work for families who do not manually open an account.